There’s nobody more passionate than a 20-something-year-old.

But being in that decade of your life is also full of:

- Enjoying your newfound freedom,

- Wondering if you’re fitting in and doing the right thing,

- Feeling like you can either have fun or figure out the nuances of life,

- Being happy, confused, and lost in a crowd that feels the same exact thing!

In other words, your 20s are a nerve-wracking learning curve. This is especially true when it comes to finances and your relationship with money. You learn to spend smartly, save and invest and so much more.

To help you stay away from financial mistakes young adults make, I’ve created this list of 20 most important money lessons to learn in your 20s. With these financial tips and advice, you get to learn what most of us did the hard way!

1. Set a financial goal

You’re probably new to making money (and figuring out what to even do with it)!

Having a financial goal in your early 20s is a game changer. Not only does it give you direction and purpose, but it also helps you avoid aimless spending.

Financial goals compel you to think beyond your immediate needs and focus on long-term planning. This way you set up your future financial security and gain perspective of your current one.

Here are some examples of financial goals you can set:

- Saving for a down payment on a home,

- Saving for educational expenses for yourself or your loved ones,

- Establishing an emergency fund (more on this later),

- Paying off high-interest debt.

2. Make a monthly budget

Creating a budget is your first step toward financial control. This straightforward yet effective tool helps you grasp your income sources and expenditure destinations.

Initiate the process by listing all your income streams– salary, side gigs, and any other earnings. Over a month, meticulously monitor expenses to get a feel of your spending habits.

Sort expenses into categories like housing, transportation, groceries, leisure, and savings. And wherever possible, keep a portion of your income separated as savings, even if it’s just 10% of your total income!

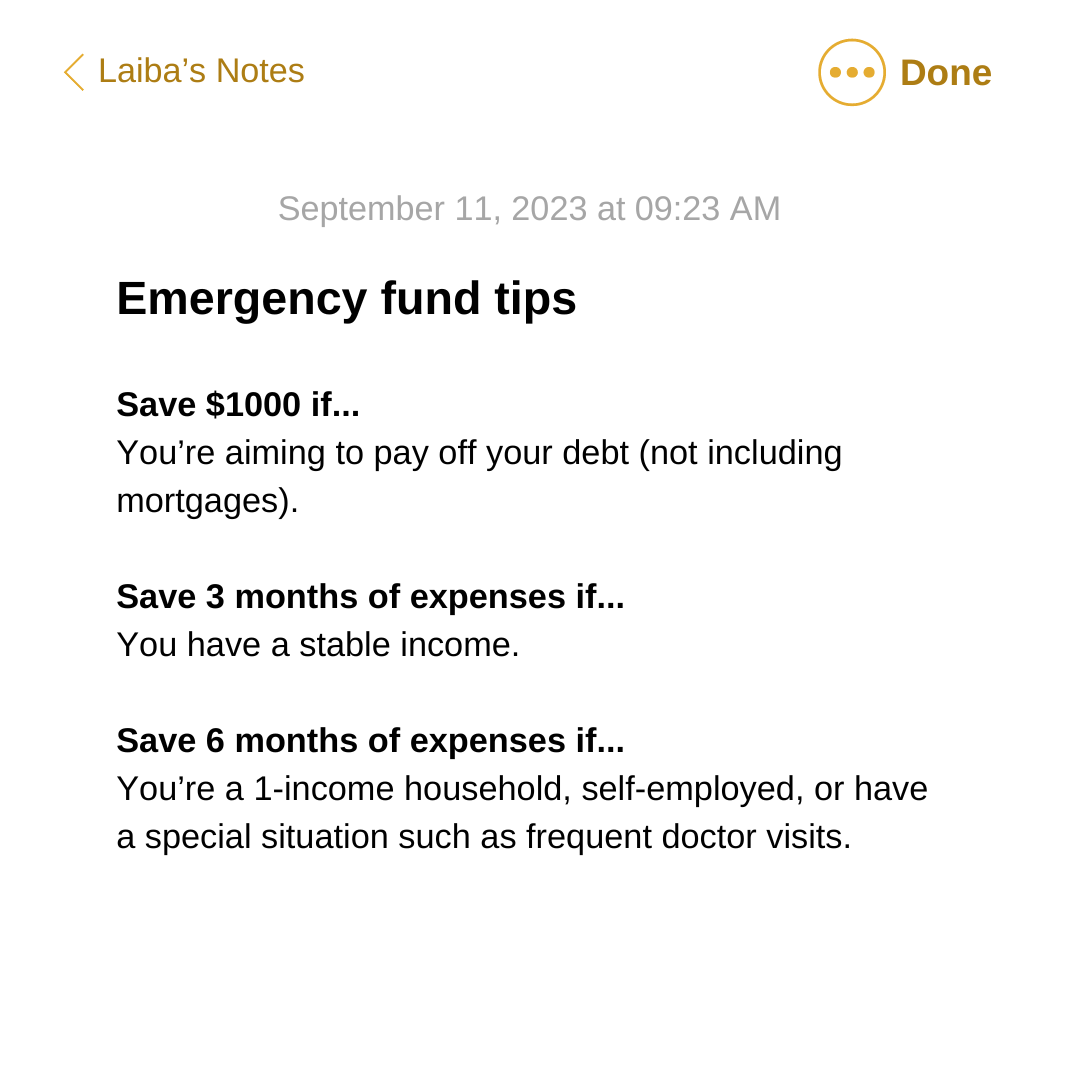

3. Create an emergency fund

In your 20s, you’re just starting your career and sometimes dealing with student loans. This makes you more vulnerable to financial shocks, compared to any other age group.

From an emergency medical situation to a broken engine, there are a lot of ways that you can feel financially incapable and stressed. And that’s exactly why you should create an emergency fund.

Emergency funds help you gain financial stability, deal with any unforeseen problems, and gain financial freedom along the way.

Tip: Add a set amount to your monthly budget for emergency funds to save up approximately 6 months of your salary.

4. Stay out of bad debt

Bad debt is money that you owe to someone or a company but have trouble paying back. It usually happens when you borrow money and can’t repay it on time or in full, like a loan or credit card.

This debt can become a problem because it often comes with high fees or interest charges, making it more expensive over time. Bad debt can also harm your credit score, making it harder to borrow money or do certain things like renting an apartment.

Without bad debts consuming your income, you’ll be better prepared to handle unexpected financial emergencies, such as medical bills or car repairs, without resorting to extra borrowing. Money that goes toward paying off bad debts could otherwise be invested to build wealth as well!

So if there’s one financial habit to avoid like the plague, it’s bad debt!

5. Don’t live beyond your means

Let’s be honest, we’ve all been tempted to make those unjustified purchases just because we had all this new money in our bank. For me, it was often fast fashion dresses to the point I felt like I might need to buy another closet for everything I was buying!

But let me remind you that living beyond your means is the opposite of being financially smart. Instead, if you want to buy something, ask yourself this: Can I afford to buy this 3 times consecutively right now?

If the answer is no, don’t buy it!

6. Retirement savings start today

Don’t think that retirement planning starts when you’re 35. Or 40.

The longer your money is invested, the more time it has to grow through compounding. Even small contributions in your 20s can potentially grow into a substantial retirement nest egg by the time you retire.

Set up automatic contributions from your paycheck or bank account to ensure consistent savings to your Roth IRA or 401(k). Or build a diversified portfolio of stocks, bonds, and other assets within your retirement accounts to manage risk.

And if your employer offers a 401(k) match, contribute enough to get the full match—it’s essentially free money.

7. Save, save, and save

As a kid, toys were your best friends. As an adult, savings are.

Your 20s are the ideal time to start saving money for different aspirational goals. Whether the savings are for your emergency fund, a Roth IRA, or paying off your debts, savings can come in handy for more situations than one.

Just make sure your saving goals are attainable!

8. Diversify your income

Your income should never be tied to just one place. And the one thing rich people do that separates them from the crowd is this:

They diversify their income sources.

So as you’re in your 20s, try your hand at different ways to earn more money. Buy a vending machine for a public place, rent out your extra room, start a drop-shipping store, invest in stocks or your friend’s new business! The sky is your limit…

9. Learn about taxes

I thought my school should have taught us about taxes more than it taught us to calculate the molecular mass in chemistry.

Here’s what I know now. Learning taxes is perhaps one of the most common money lessons for young adults that financial experts give!

Knowing what you can write off as tax deductions, important tax forms, and accounting mistakes that can cost you more in taxes, you can be cost-effective and smart during tax time.

10. Invest to grow your wealth

Generally, people in their 20s can afford to take on more investment risk because they have a longer time to recover from market fluctuations.

But starting early in the investment side of money also gives you more time to compound your investments and enjoy a larger payout than if you do it at 30!

Investing can help you achieve important financial goals, such as buying a home, starting a business, or saving for retirement. The sooner you start, the more time your investments have to work toward these objectives.

11. Pay off your credit card bill every month

Credit cards are notoriously handy. If your paychecks are tight, you can quickly swipe your card to get what you want or need without a question. However, it’s exactly that easy to spiral out of control.

Your 20s are the foundation of your financial life. So, be careful and pay your balances in full every month to create a favorable credit score.

If you ignore credit card bills for too long, you’ll quickly be in debt with an absurd interest rate, and it will most likely take longer to pay them off than if you had just used the money you had! Also, avoid opening multiple lines of credit.

Tip: Don’t use credit if you don’t have the money in your checking account.

12. Grow your financial knowledge

Your relationship with money is ever-growing, and there are many reasons why you should invest in your financial knowledge.

Many individuals in their 20s may have student loans, credit card debt, or other financial obligations. The only way to get out of that hole is to expand your financial knowledge because when you are equipped with wealth-building strategies and financial planning, you can make informed decisions to change your life.

I recommend going down a combination of these routes to establish a strong financial foundation and expand it:

- Reading books on financial literacy, personal finance, and wealth strategies,

- Joining local investment clubs,

- Learning about tax laws and strategies,

- Read personal finance blogs (you’re already here),

- Seek professional advice from CFOs!

13. Maintain proper insurance

Being young doesn’t mean you’re invincible. You can always come down with an emergency that strains your finances.

According to a report, 40% of Americans can’t tolerate a $400 setback and can fall back on paying their bills.

And so, Business Insider says that not signing up for proper insurance is one of the biggest money lessons for young adults in today’s age. If anything happens, your cost setback is much lower, and you don’t sacrifice quality healthcare over a lack of money!

14. Check your credit report regularly

Your credit report is directly related to your credit score and financial future. By monitoring your credit report, you can ensure that it accurately reflects your financial behavior, including on-time payments and responsible credit usage.

This helps in building and maintaining a positive credit history. Lenders and landlords often check your credit report to assess your creditworthiness.

So, this report is essential if you want to get loans, credit cards, and even rent an apartment!

15. Negotiate how much you get paid

Did you know that 85% of Americans who negotiated their salaries were successful?

The salary you earn early in your career often sets the baseline for your future earnings. Negotiating a higher starting salary can lead to higher raises and bonuses over time, which can significantly impact your long-term financial well-being.

It can help you cover your living expenses, save for the future, and repay any student loans or debts more comfortably. You can also enjoy a larger retirement payout from your saved funds!

But this doesn’t just affect your current job! You can expect increased pay at future jobs, since employers often base offers on your previous salary.

16. Spend on experiences, not material things

It’s impractical if anyone suggests that your 20s should be all money-saving and not blowing it. So when your life calls for a vacation or getaway, ensure you’re spending the amount on an experience and not just a material thing.

This way, when you look back on the money that isn’t in your account anymore, you have a memory to replace it. Just like a transaction!

17. Talk about financial expectations with your partner

According to Match.com, at least 50% of people found their partners in their 20s.

So if you find yourself in a serious relationship, sit down to discuss your finances with your partner. It’s crucial that both of you know each other’s income and debt levels. You also need to talk about whether your household will have separate bank accounts or open a joint one!

Remember that when you’re picking your partner, financial compatibility plays a huge role in how everything turns out.

18. Self-awareness is key to self-success

Realizing your financial situation takes you one step closer to improving it. And your 20s will be all about trial and error, even in financial aspects!

So throughout the process, be honest with yourself on what financial habits are improving your life and what are detrimental to you. Then take corrective steps to get better next time around.

Remember, don’t make the same mistake twice! Be creative.

19. Don’t follow all money lessons and advice

There will be a lot of financial experts there.

From your uncle who lost money on real estate in Milwaukee to friends who maxed out multiple credit cards and are in crippling debt now, you’ll hear tons of financial advice.

And you should listen to all of them but follow a few of them.

20. Don’t compare yourself

This might sound like a line from a mental health brochure. But to financially succeed, this money lesson for young adults goes a long way.

Some people around you will act like they have it all figured out. Some will be substantially wealthy and advancing in their careers fantastically.

There will also be people who won’t be doing well and use you as a financial crutch. There will also be people who won’t let you know that their career goals are failing.

Don’t compare yourself. Financial and career journeys aren’t the same for anyone. Focus on what your financial goal is and what you can do to reach there faster and with stability.

Destress Financially With Stanton Financial Co.

If you want to dive head over heels into being the creative mastermind of your brand, Stanton Financial Co. can help you.

Stanton Financial Co. is a premium bookkeeping and CFO service that brings big business strategies to small businesses, solopreneurs, influencers, and content creators.

Unlike most bookkeeping services, we make it easy for you to profitably manage your fluctuating income. Collaborate with brands and focus on doing what you do best– we’ll take care of everything else!